01 Apr SaaSpocalypse and More – 2026 Q2 Commentary

The first quarter of 2026 began with several sources of stock market volatility including what pundits have described as the SaaSpocalypse. SaaS stands for software as a service. For years, companies that employed a SaaS business model thrived in terms of profitability and stock market performance. However, during the first quarter, the market started to question whether Artificial Intelligence (AI) driven agents could easily replace some of the functions of software that these SaaS companies provide. One example would be Intuit Inc. (ticker: INTU), which sells the TurboTax product. INTU’s share price is down 37% year-to-date because the market believes AI agents will take over the work of tax preparation. We present INTU as one example, but we see many others in the market including some names in our portfolio. We highlight the “SaaStrophe,” but several other factors have helped drive volatility in the early part of the year. We will list those below and briefly discuss each.

Early 2026 Volatility Drivers

- SaaSpocalypse

- Private Credit

- War in Iran

- Ongoing tariff questions

We list the fear around software stocks and AI’s effect on them first because that question from the market will not resolve in the next six months. We foresee an ongoing debate until we get a few quarters of results from these businesses while either competing with or employing AI. We currently have the in-house view that AI will lead to winners and losers in the software sector. Software that offers a high trust service could maintain its position of relevance, while more commodity-like functions risk displacement. We have long had a significant amount of cybersecurity exposure in the portfolio. Today the market questions whether AI could replace those businesses. We believe the trust level between enterprises and their cybersecurity providers has to be at such a high level that enterprises would have a difficult time passing cybersecurity tasks off to an unchecked AI agent. In fact, we just invested in a cybersecurity company that has AI agent identity verification as part of its enterprise cybersecurity business. The stock of the company had fallen significantly during the SaaSpocalypse, and we think the business just described will grow, not shrink as a result of the proliferation of AI agents. The question of AI will linger for several quarters and likely years. We will continue to evaluate the opportunities created by the market’s questions, and look to take advantage of the current and future volatility. Private Credit, number two on the list above, refers to the concern that loans issued by so-called private credit companies are starting to go bad and retail investors cannot get their money out of the funds that have been created to hold these loans. The financial services industry created the euphemism “interval funds” to describe these funds. Interval refers to an investor’s ability to redeem shares in these funds on an interval, typically a couple of days each quarter. We have had a number of clients come to us from other advisors who have stuffed their portfolios with these private credit interval funds. We use the term stuff because typically these funds are higher fee and have not performed appreciably better than holding an allocation of bonds and money market funds. The reason we do not want to hold these types of funds is their lack of liquidity and we believe we can achieve the potential diversification benefit in other ways. Also, it has tended to take a couple of years to fully get our clients out of one of these investment vehicles.

The interval nature of the private credit funds in the news at the moment should not surprise investors. Those gates existed before any turmoil in the industry. What has increased the focus on private credit is that a significant percentage of the loans made by private credit providers have been to software businesses. As mentioned above, AI has called into question the validity of those businesses going forward. You can see in Graph 1, below, the interest rates on software loans increased significantly at the beginning of February of this year. That increase has created pressure on the private credit funds introduced above. Whether the funds actually face more loan defaults within them or investors want out due to perceived increase in defaults, it almost does not matter because the news flow has led to a “run” on these funds. Private credit providers stepped into a void after the Great Financial Crisis (housing crash) when banks became restricted from making certain types of loans. For that reason, we do not see the current pressure on private credit leading to some sort of systemic problem. We do think this issue has a more limited lifespan than the aforementioned SaaSpocalypse. However, issues within the private credit market could lead to greater corporate liquidity issues, which could lead to less available funding for the AI buildout and one of the key drivers of market performance since 2022, when ChatGPT became available for public use. We continue to monitor the situation intensely, and look for opportunities created by this volatility.

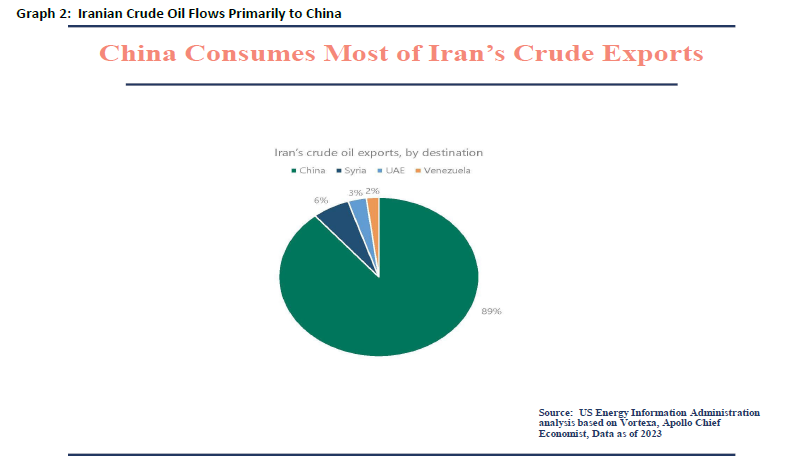

The launch of missiles at Iran by the United States and Israel in February has turned into an ongoing war that has blocked the Strait of Hormuz. The strait is a narrow waterway between the Persian Gulf and the Gulf of Oman. Approximately 20% of the world’s oil liquids consumption passes through the strait. As we write, the threat of force from Iran, directly north of and abutting the strait, has put Iran in effective control of the strait. We already see the impact of this in terms of long queues for fuel in some Asian countries that rely on the Gulf States for oil supply. The global supply chain disruption from an ongoing war between the US and Iran could lead to inflation similar to what we observed during the Covid-19 pandemic. Oil and oil and gas-related byproducts are used as inputs in many goods, so a diminished flow of oil and gas will lead to higher costs of goods – or inflation. Unlike the SaaSpocalypse and issues in private credit, we see the Iranian conflict as having a more limited duration. We anticipate too many nations interested in getting the Strait of Hormuz running again. For example, in Graph 2, below, you see that China consumes 89% of Iran’s crude oil exports. Iranian oil constitutes a significant source of Chinese oil, with estimates that 8% to 10% of Chinese oil consumption comes from Iran. We do not think the Chinese nor the Iranians will want to limit that flow for long.

Despite our current view on the longevity of the war, any length measured in months instead of days will disrupt supply chains and lead to inflation. We prepared a little for this type of event by coming into 2026 with 10% of the portfolio invested in oil and gas companies. The share prices of those companies have performed well this year, but not in a way that offsets the overall market volatility. Energy companies had improved their businesses, become more capital efficient, and their stocks looked cheap. A geopolitical hedge remains an added benefit of investment in that sector. An investment manager needs to try to get ahead of events like the Iranian war. Pivoting the portfolio to more war hedges now would likely come too late to have a meaningful effect. We hope the war concludes and the world can move forward in peace.

We would not describe the tariff situation as peaceful. On February 20th, the US Supreme Court ruled that International Emergency Economic Powers Act (IEEPA) does not authorize the president to impose tariffs. In theory, all the tariffs enacted almost a year ago under IEEPA would need to be repealed and refunded. This process will create headaches and the Administration will try to find ways to maintain the impact of the tariffs while working around this ruling. In our opinion, the market impact of tariff headlines has declined and of the four items listed above driving market and economic volatility, we would put tariff news as the fourth most important.

If one removed the Iran War and tariff news, the SaaSpocalypse and private credit concerns amount to enough to drive significant market volatility. Graph 3, below, demonstrates that volatility within the S&P 500 constituents certainly increased during February 2026. This graph shows the percentage of constituents with an absolute one-day move greater than 10%. While not the same level of single stock volatility as when the Administration originally announced tariffs in April of 2025, the number of stocks moving more than 10% increased. That illustrates the current market environment, which presents a challenge to manage through. We understand it can be very stressful to log into your accounts and see the kind of share price movements associated with the environment we have described above. However, we constantly prepare our “shopping list” in order to be ready for these types of market dislocations. We have made some portfolio changes, and would expect to make more if the volatility persists. We find ourselves in another time where “volatility provides opportunity.” However, if you find yourself in or near a distribution phase of life, or if you have a large expense that we do not know about, please contact us.

We want to thank you for your trust and ongoing support. We understand that this type of market and economic environment leads to more questions than usual. Please reach out with any questions. We want to chat with you and do not consider contact for any reason to be an inconvenience. Our goal is to protect and grow your assets – a mission we take very seriously. Have a wonderful spring.

Sorry, the comment form is closed at this time.